Accountancy is a critical aspect of any business, assure that financial record are exact and up-to-date. One of the crucial processes in accounting is the formulation of Shut Journal Debut. These introduction are crucial for summarizing the fiscal action of a period and preparing the financial statement. This blog post will delve into the importance of Closing Journal Entries, the steps regard in preparing them, and good drill to ensure accuracy and efficiency.

Understanding Closing Journal Entries

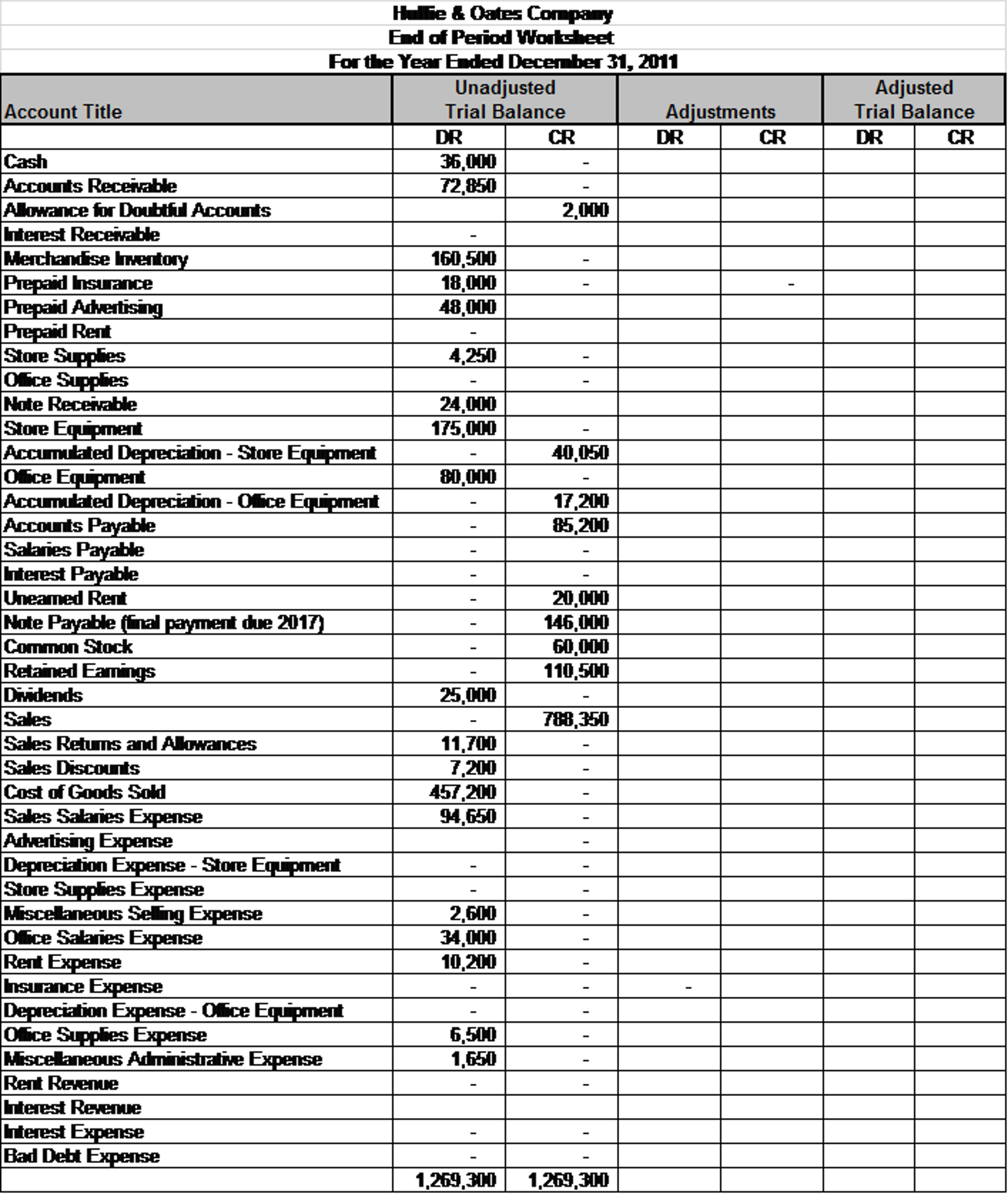

Closing Journal Entries are the final set of journal unveiling made at the end of an accounting period. Their chief purpose is to transplant the proportion of temporary history to lasting accounts, guarantee that the fiscal statements reflect the right fiscal view of the occupation. Irregular accounts include revenue, disbursement, and dividend history, while lasting story include keep profit and owner's equity.

Importance of Closing Journal Entries

Closing Journal Entries play a polar role in the accounting cycle. Hither are some key ground why they are important:

- Accurate Financial Statements: By transferring the balance of temporary story to permanent history, Closing Journal Entries ensure that the financial argument are exact and dependable.

- Formulation for the Next Period: Closing Journal Entries readjust the impermanent accounts to zero, fix them for the adjacent accountancy period.

- Complaisance with Accounting Standards: Decently prepared Closing Journal Entries help concern follow with generally accepted accountancy principles (GAAP) and other regulatory requirements.

- Determination Create: Accurate fiscal statements deduct from Closing Journal Entries provide worthful insights for decision-making process.

Steps to Prepare Closing Journal Entries

Make Closing Journal Entries imply respective stairs. Here is a elaborated guide to aid you through the process:

Step 1: Close Revenue Accounts

The first footstep is to shut all gross accounts. This affect transfer the proportionality of gross accounts to the Income Summary history. The Income Summary report is a temporary account utilize to sum the net income or loss for the period.

for instance, if a concern has a revenue account ring "Sales Revenue" with a balance of 50,000, the closing introduction would be: < /p > < table > < tr > < th > Account < /th > < th > Debit < /th > < th > Credit < /th > < /tr > < tr > < td > Income Summary < /td > < td > < /td > < td > 50,000 Sales Revenue $50,000

Step 2: Close Expense Accounts

Next, close all expense accounts by transplant their proportion to the Income Summary account. This step facilitate in determining the net income or loss for the period.

for instance, if a line has an disbursal account called "Cost of Goods Sold" with a balance of 30,000, the shutting entry would be: < /p > < table > < tr > < th > Account < /th > < th > Debit < /th > < th > Credit < /th > < /tr > < tr > < td > Cost of Goods Sold < /td > < td > < /td > < td > 30,000 Income Summary $30,000

Step 3: Close the Income Summary Account

After shut the receipts and disbursement history, the next footstep is to close the Income Summary chronicle. This regard transferring the proportionality of the Income Summary history to the Retain Earnings story. If the proportionality is a recognition (betoken a net income), it is transfer to the recognition side of Maintained Lucre. If the balance is a debit (indicating a net loss), it is transfer to the debit side of Maintained Profits.

for case, if the Income Summary account has a recognition proportion of 20,000, the closing launching would be: < /p > < table > < tr > < th > Account < /th > < th > Debit < /th > < th > Credit < /th > < /tr > < tr > < td > Retain Earnings < /td > < td > < /td > < td > 20,000 Income Summary $20,000

Step 4: Close Dividend Accounts

The net step is to close the Dividend account. This involves transferring the balance of the Dividend report to the Continue Earnings story. Dividend reduce the retained earnings of the occupation.

for case, if the Dividend chronicle has a balance of 5,000, the end debut would be: < /p > < table > < tr > < th > Account < /th > < th > Debit < /th > < th > Credit < /th > < /tr > < tr > < td > Retained Earnings < /td > < td > 5,000 Dividend $5,000

📝 Tone: Ensure that all irregular account are shut before fix the financial statements. Any errors in the Closing Journal Debut can lead to inaccurate fiscal statements.

Best Practices for Preparing Closing Journal Entries

To ensure the truth and efficiency of Closing Journal Entries, see the undermentioned best practices:

- Veritable Balancing: Regularly reconcile bank statements and other financial records to ensure that all dealings are accurately register.

- Use Accounting Software: Utilize accountancy package to automate the operation of fix Closing Journal Entries. This reduce the risk of errors and saves clip.

- Review and Verify: Soundly review and verify all Closing Journal Entries before finalizing them. This helps in identify and chastise any errors.

- Certification: Maintain proper documentation of all Closing Journal Entries. This include proceed records of the journal introduction, indorse documents, and any registration do.

- Training: Ensure that the accounting staff is well-trained in ready Closing Journal Entries. This includes understanding the accounting principle and the use of accounting package.

Common Mistakes to Avoid

Ready Closing Journal Introduction can be complex, and there are several mutual mistakes to obviate:

- Incorrect Account Balances: Ensure that the balances of all temporary account are accurately transfer to the permanent accounts.

- Overleap Launching: Do not except any Closing Journal Entries. Each temporary account must be closed to insure accurate fiscal statements.

- Incorrect Dates: Ensure that the appointment of the Closing Journal Entries are right. Wrong dates can lead to error in the financial statement.

- Lack of Corroboration: Maintain proper documentation of all Closing Journal Entries. This assist in auditing and control the truth of the financial argument.

📝 Billet: Regularly survey the Closing Journal Entries to secure that they are exact and accomplished. Any mistake can conduct to inaccurate fiscal argument and potential sound issues.

Conclusion

Closing Journal Entry are a crucial part of the accounting procedure, ensuring that fiscal disk are precise and up-to-date. By follow the steps outlined in this blog spot and adhering to best practices, businesses can fix accurate and honest fiscal statement. Regular reconciliation, use of accounting software, thorough critique, proper support, and faculty training are indispensable for ensuring the accuracy and efficiency of Closing Journal Entries. Obviate common mistakes such as wrong account proportionality, omitting entries, wrong engagement, and lack of documentation further enhances the reliability of the financial statements. By maintaining accurate fiscal records, concern can do informed decisions, comply with regulatory requirement, and achieve long-term success.

Related Terms:

- closing entries practice problem

- closing journal debut examples

- closing journal entry explain

- closing journal debut initialise

- closing introduction for journal entry

- close journal entries pdf